Weekly Brief #38

Amazon’s 8% drop, explained...Magnificent 7 Q2 earnings (cont.), Leader of Hamas killed in Iran, CrowdStrike slapped with lawsuit(s), Deadpool 3, highest grossing rated-R movie, Venezuela elections.

Good morning investors 👋,

Happy Friday and welcome, or welcome back, to the 38th Weekly Brief.

Summer Olympics 2024 kick off: The Olympics Games Paris officially started last Friday, and the medals have started to rake in. Canada is ranked 9th out of 204 countries and territories competing this year based on the amount of gold medals (at the time of writing). And in economic news, the Fed is ‘locked and loaded’ to cut rates in September according to Reuters, with the next Fed meeting scheduled 7 weeks before the U.S. presidential election.

Let’s get into it.

In this issue:

📉 Amazon’s 8% drop, explained

💰 Magnificent 7 Q2 earnings (cont.)

🇮🇷 Leader of Hamas killed in Iran

FEATURED STORY

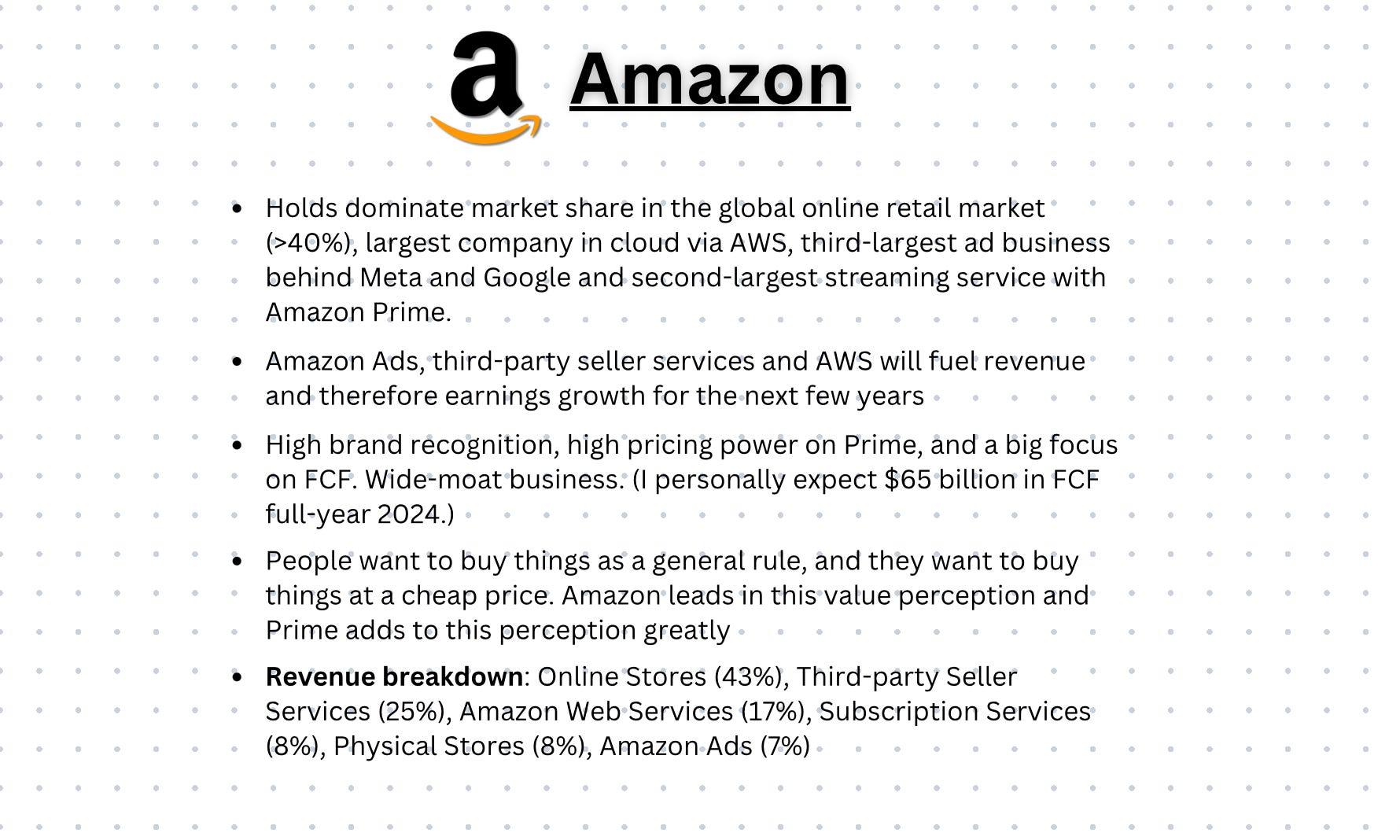

📉 Amazon’s ~8% drop, explained

Yesterday (Aug 1, 2024), Amazon released its Q2 2024 earnings results. It was pretty mixed, with a miss on the top line and a 22% beat on the bottom line. There’s more to the story, which I’ll discuss below, but overall, it led to an 8% selloff in after-hours trading.

Why did Amazon sell off? Let’s take a brief look at Amazon’s key earnings metrics and its major growth revenue segments (Ads, AWS, third-party seller services) for this quarter:

Earnings per share: $1.26 vs. $1.03 expected.

Revenue: $147.98 billion vs. $148.56 billion expected.

AWS (Amazon Web Services): $26.3 billion vs. $26.0 billion expected. (17% year-over-year growth.)

Amazon Advertising (Twitch, Prime Video etc.): $12.8 billion vs. $13 billion expected. (20% year-over-year growth.)

Third-party seller services (fulfilled by Amazon): $36.2 billion vs. $36.5 billion expected. (12% year-over-year growth.)

Averaged together, Amazon’s high-margin businesses — its intrinsic value drivers — based on this quarter, have grown at over 16% year-over-year. This, paired with trailing twelve-month (TTM) free cash flow (FCF) of $52 billion, means this wasn’t a really bad earnings report. All of Amazon’s major (most important) revenue streams are growing incredibly. Amazon still holds its dominant market share in cloud with AWS, is continuing to grow its advertising business, which is the third-largest in the world, and continues to increase its FCF.

For perspective, the TTM number of FCF this quarter, based on simple math (past two quarters of FCF divided by two, times four), suggests that Amazon could potentially be on track to produce $104 billion in FCF this year. (Personally, however, I believe $65-70 billion in FCF is much more reasonable.)

So, why is Amazon down? It’s a combination of a miss on revenue expectations, slower advertising growth than expected (21% growth expected as opposed to 20%), and weaker Q3 guidance than anticipated. At least that’s what I believe.

Do these quarterly expectations matter long-term? Not at all. Is Amazon continuing to grow its major high-margin revenue streams? Yes. Is Amazon focused on producing massive amounts of FCF? That’s what it seems to me. If Amazon had beat on revenue and grown advertising 1% more, along with other minor improvements, it would have seen a nice boost in stock price. But it didn’t meet those expectations from analysts, and the stock is down 7%.

Justified sell-off? Probably not. But the stock market is an analyst’s game quarter-by-quarter and an investor’s game year-by-year. It’s all about the long term, buying sustainable businesses and letting those businesses yield fruits. I focus on the long term, and long term, Amazon is the best it’s ever been.

So in short, I’ll be buying.

I’m still holding (and buying)

Amazon is never at the forefront of “tech” stocks. When it comes to “big tech,” they’re only included in that category because they’re such an unusually large company by market cap. Usually, “big tech” refers to Microsoft, Apple, or Google, all of which I believe are currently overvalued.

Big tech companies are the greatest on earth. They have the largest amounts of FCF, net income, and the deepest, widest moats or competitive advantages. Buying big tech stocks has historically been expensive, but these stocks have delivered the highest returns. That’s because they’re such amazing businesses and have zero to no competition.

The thing is, at the forefront of AI and that whole situation, Apple, Microsoft, Nvidia, and Google are being traded up like crazy. (I personally believe the trade-up in Apple is justified because the iPhone sales of Apple Intelligence aren’t speculative, but anyway.)

Amazon is the outlier here, in my opinion. Investors don’t believe Amazon is an AI play, so Amazon hasn’t experienced that sort of ‘AI overvaluation,’ if you will.

Yet, Amazon is still a part of big tech because it’s such an amazing business. A company that controls such a dominant share in what I believe to be very valuable industries (e-commerce, online advertising, cloud computing). Amazon is also trading at historical lows (based on OCF multiples), growing FCF at double digits, growing earnings in the high teens, and continuing to grow their already amazing top line at consistent double digits powered by growth in advertising, AWS, third-party services, and subscription revenue.

I share my rough thesis on why I’m buying and continuing to hold Amazon stock on my Blossom Social account. If you want, make sure to check that out here.

FINANCE

💰 Magnificent 7 Q2 earnings (cont.)

Meta, Amazon, and Apple all reported their quarterly earnings results this week. Here’s how that went (brief overview):

AMZN Q2 2024:

Earnings per share: $1.26 vs. $1.03 expected.

Revenue: $147.98 billion vs. $148.56 billion expected.

AWS: $26.3 billion vs. $26 billion expected.

Advertising: $12.8 billion vs. $13 billion expected.

Net income was $13.5 billion, or $1.26 per share, up 101% from $6.7 billion, or $0.65 per share a year ago. Revenue rose 10% to $148.0 billion from $134.4 billion the previous year.

AAPL Q3 2024:

Earnings per share: $1.40 vs. $1.35 expected.

Revenue: $85.78 billion vs. $84.53 billion expected.

iPhone: $39.30 billion vs. $38.81 billion expected.

Mac: $7.01 billion vs. $7.02 billion expected.

iPad: $7.16 billion vs. $6.61 billion expected.

Wearables, Home, Accessories: $8.10 billion vs. $7.79 billion expected.

Services: $24.21 billion vs. $24.01 billion expected.

Net income was $21.45 billion, or $1.40 per share, up 8% from $19.88 billion, or $1.26 per share a year ago. Revenue rose 5% to $85.78 billion from $81.80 billion the previous year.

META Q2 2024:

Earnings per share: $5.16 vs. $4.73 expected

Revenue: $39.07 billion vs. $38.31 billion expected

Family daily active people (DAP): 3.27 billion on average for June 2024, an increase of 7% year-over-year.

Net income was $13.47 billion, or $5.16 per share, up 73% from $7.79 billion, or $2.98 per share a year ago. Revenue rose 22% to $39.07 billion from $31.99 billion the previous year.

BUSINESS

🖥️ CrowdStrike slapped with lawsuit(s)

CrowdStrike is now being sued by its very own shareholders after a faulty software update crashed over 8 million computers, disrupting businesses, including airlines, banks, and hospitals. Delta Air Lines reported that the outage cost the airline $500 million in lost revenue and compensation. (Delta is also suing CrowdStrike.) After the failed update, CrowdStrike’s share price fell more than 32% in 12 days, losing over $25 billion in value.

The lawsuit, filed in Austin, Texas, alleges executives defrauded investors by claiming the software updates were adequately tested. The suit seeks compensation for investors who held shares between November 29 and July 29. CrowdStrike denies the allegations stating that the affected computers were back to normal as of July 29, ten days after the incident.

🍿 Deadpool 3, highest grossing rated-R movie

Marvel Studios’ Deadpool & Wolverine had a record-smashing opening weekend, earning $444.1 million globally, with $211 million in the domestic box office. This makes it the highest-grossing global opening for an R-rated film in history, surpassing the previous record which was the first Deadpool (2016).

Domestically, it was the 6th highest-grossing opening of all time and the highest July opening weekend ever, surpassing the live-action Lion King (2019). The Walt Disney Company, parent of Marvel, has now released the No. 1 films for May (Kingdom of the Planet of the Apes), June (Inside Out 2), and July (Deadpool & Wolverine), now holding 5 of the top 6 opening weekends of all time.

🇮🇷 Leader of Hamas killed in Iran

Ismail Haniyeh, Hamas’ top leader, was killed in an Israeli airstrike in Tehran early this Wednesday at the age of 62. Haniyeh, who was on Israel’s hit list after Hamas’ Oct. 7 attacks, was killed at his residence in Tehran after attending Iran’s new president’s swearing-in ceremony.

Haniyeh had been living in exile in Qatar since 2019, traveling to Turkey and Iran for negotiations. His role in Hamas’ leadership also led to personal losses, with an Israeli airstrike killing three of his sons and other relatives. Despite being detained by Israeli authorities in 1989, he continued to rise in Hamas, eventually serving as Gaza’s prime minister after Hamas won legislative elections in 2006.

Iran has said they plan on retaliating against Israel for the killing.

📚 Book of the Week

Note: I don’t recommend books that I haven’t read or that I would never read. The books I recommend are books I have already read or that I will eventually read.

Surrounded by Idiots — Thomas Erikson

Book Description:

You are not alone. After a disastrous meeting with a highly successful entrepreneur, who was genuinely convinced he was ‘surrounded by idiots’, communication expert and bestselling author, Thomas Erikson dedicated himself to understanding how people function and why we often struggle to connect with certain types of people.

Surrounded by Idiots is an international phenomenon, selling over 1.5 million copies worldwide. It offers a simple, yet ground-breaking method for assessing the personalities of people we communicate with – in and out of the office – based on four personality types (Red, Blue, Green and Yellow), and provides insights into how we can adjust the way we speak and share information.

Erikson will help you understand yourself better, hone communication and social skills, handle conflict with confidence, improve dynamics with your boss and team, and get the best out of the people you deal with and manage. He also shares simple tricks on body language, improving written communication, advice on when to back away or when to push on, and when to speak up or shut up. Packed with ‘aha!’ and ‘oh no!’ moments, Surrounded by Idiots will help you understand and communicate with those around you, even people you currently think are beyond all comprehension.

And with a bit of luck you can also be confident that the idiot out there isn’t you!

✩ This newsletter, along with my weekly Morningstar fair value estimates and PDFs, will always be free of charge. Your support, whether through a donation or by reading this newsletter and following along, is greatly appreciated.

Thank you for reading today’s Weekly Brief! If you enjoyed or learned anything, please spread the word.

— Jacob