Acquiring Shareholder Returns

Constellation Software (CSU.TO) stock analysis: A quality Canadian software behemoth trading at historic lows

When I was 7-years-old (in or around), my brother slammed a thick bedroom door on my right big toe. A door the thickness of ten Kit Kats, mind you.

Thud! There went my toenail.

I immediately ran to the nearest parent to get my brother in trouble, tears in my eyes like the Oscar winner I am, who sat me down and quickly bandaged me up. Kids being kids, we were probably fighting over a toy now meaningless to our older selves, though me and my toe have never felt better since.

In the case of a quality Canadian tech behemoth like Constellation Software, the market has repeatedly slammed a metaphorical door on its stock price, now down 50%+ from its highs, driven by AI concerns that “vibe coding” will replace traditional software.

Constellation, being a unique business that requires other software companies operating smoothly for it to operate smoothly (this sentence will make sense in a bit), was hit quite hard.

And so, I wanted to fully cover Constellation, a quality company now at an historically low price, to answer whether or not these AI concerns are overblown, and whether it’s worth a buy.

Business model & analysis

Constellation Software Inc. (also “CSU” or “CSI”), is a Canadian diversified software company based in Toronto, Ontario, describing itself as an “international provider of market leading software and services.”

Revenue breakdown

Constellation earns its revenue from four segments (as of Q3 2025):

Maintenance and other recurring (75.1% of revenue): Traditional subscription and subscription-type revenue. Recurring, typically high-margin revenue from offering software access (SaaS).

Professional services (18.3% of revenue): The implementation, customization, consulting, and other services to help setup, deploy and integrate Constellation’s software into the workflow of a particular business.

License (3.6% of revenue): One-time software license fees. Now mostly legacy revenue as most software has shifted to a subscription model1.

Hardware and other (3.0% of revenue): Physical sales of hardware bundled or sold alongside software in certain offerings. Think of point-of-sale systems for retail (Square, Shopify POS), or other equipment typically paired with software.

Revenue by region (as of FY 20242):

United States (45% of revenue)

UK/Europe (33% of revenue)

Canada (9% of revenue)

Rest of World (13% of revenue)

Note: Plenty of times in this analysis, I use “CSU” (Constellation’s ticker) or “CSI” (abbreviation of ‘Constellation Software Inc.’) as shorthand instead of the full “Constellation.” Something worth keeping in mind.

Business model

Constellation Software is a software company with a business model that relies on acquiring a specific type of software company. These specific software companies it acquires, then, in turn, help Constellation acquire more of that specific type of software company. That’s the model.

While these past few sentences seem like an unintelligible ramble, I can assure you, not all of it was.

CSU is what’s known as a “serial acquirer,” a company that grows primarily through the continuous acquisitions of othercompanies rather than its own organic growth. Serial acquirers usually specialize in acquiring companies operating in specific segments or industries, rather than buying everything with a SaaS model that sees light. And CSU is no different from this.

Constellation, like many with a similar business model, is a niche serial acquirer, specializing in the acquisitions of Vertical Market Software (VMS) companies.

In software, there are two types of broad classifications of what software is, and this varies based on what market it serves, and how.

To understand, picture yourself as Bill Gates in the early 80s, creating what would eventually be the world’s spreadsheet: Microsoft Excel. Unknowingly, you would be creating what’s known as Horizontal Market Software (HMS), a type of software widely applicable across many industries and domains, typically with a large addressable market.

Excel, like Microsoft Word (and even Salesforce CRM or Adobe Creative Cloud), are broad, “anyone can use it” piece of software, and that’s what HMS is.

On the other hand, VMS (the specific type of software CSU targets to acquire) are niche, task-specific, mission-critical piece of software. That is, a piece of software vital for a company to function, and usually (in the case of CSU) operating in a very niche industry.

Example A:

“We have software that determines how much grain you would put into a truck or a railcar in the Midwest of the U.S.” — Mark Miller, President, Constellation Software

Think of graveyard plotting software, or a golf course bookings management software… these are the types of companies CSU targets; those with specialized software incredibly valuable to the client who needs it, with a very niche application. A golf course isn’t a golf course without the software to manage its bookings and tee times. At least not in a modern world. And this truth applies to every vertical product within CSU’s sphere, some more than others.

Most of CSU’s revenue is recurring, earned from the typical subscription model that most software companies use, and therefore, VMS companies use. However, because of the specialization of VMS applications, CSU also earns a large chunk of revenue to help install and set up the software for those who need it. (This second revenue stream isn’t just good for business, but is a strong argument for CSU’s advantages in an AI world. But more on this in the Risks section.)

Summarized, CSU’s model can be thought of as: (1) Buy VMS companies, (2) Repeatedly look across the market for more VMS companies, and (3) Continually acquire VMS companies at a price it deems fair using capital generated from its existing VMS subsidiaries.

In essence, it’s a VMS-buying hamster wheel, or, to most analysts, a typical flywheel model:

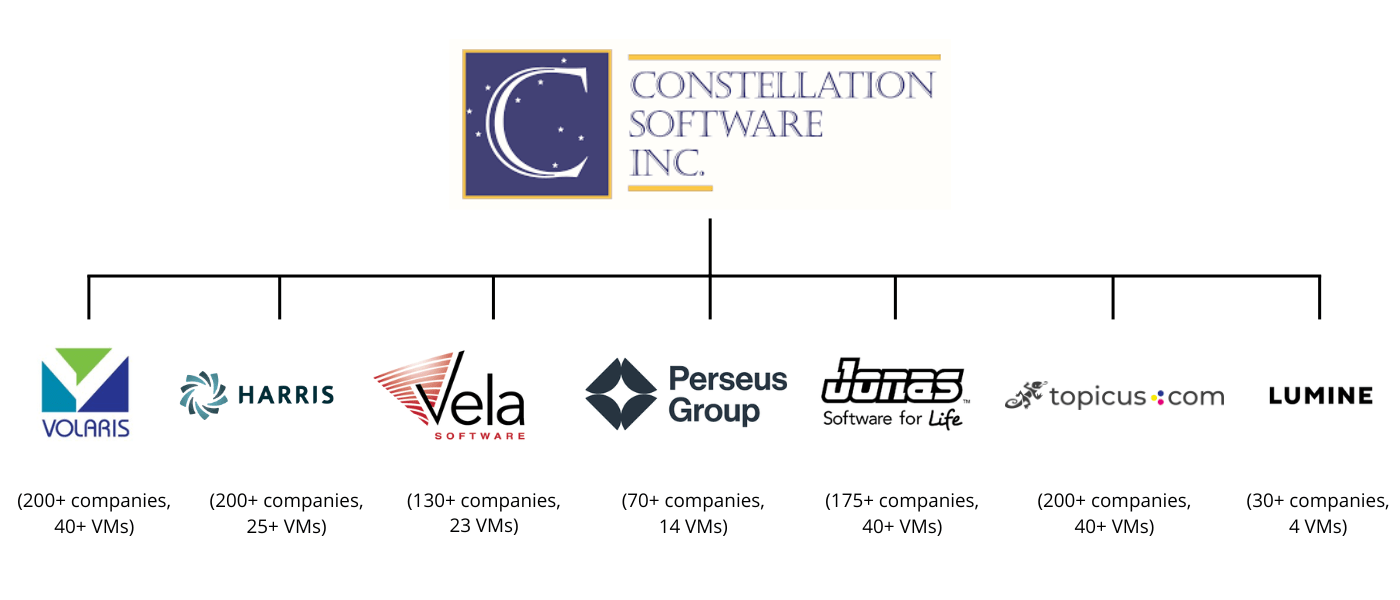

Any new VMS company purchased by CSU is usually bought by a particular unit or operating business under CSU, which is a list of 7 large companies that manage particular verticals of CSU’s VMS suite of companies.

Those companies are: Volaris, Harris, Vela Software, Perseus Group, Jonas, Topicus, and Lumine (photo below). (Topicus and Lumine are publicly-traded companies where CSU holds effective control. These can be thought of as publicly-traded subsidiaries, but more in the Financials section.)

Through these operating groups, there are multiple business units underneath (BU) that group together the specific companies within a market. CSU owns a little less than 1,000 individual companies across 150+ vertical markets.

While there are exceptions, CSU typically buys any new company through these 7 operating groups that each cover specific vertical markets. Vela Software is buying healthcare-related VMS, or Harris is buying utility-related VMS, and so forth, all through those operating groups’ BUs. (Though it’s not listed as an operating group in CSU’s reports, I consider Lumine the unofficial 7th, given the control.)

Additionally, every company CSU acquires, regardless of vertical, is heavily decentralized from the parent company. There is no integration into a single “Constellation cemetery software bundle” or anything of the sort.

Despite being an acquirer, CSU keeps its acquired companies as-is.

For example, if “Jacob’s Elevator Repair Software” was bought by CSU, it continues to be “Jacob’s Elevator Repair Software” until the end of time. Maybe the name could change, but management, all employees, and more, stay as they were before the acquisition.

CSU’s serial acquirer model allows its subsidiaries to remain independent even while being… well, subsidiaries. This gives CSU some clout when scouting future VMS buyouts. In fact, CSU has a reputation in the industry for being a “forever home” for software companies, which shows the positive working culture and feedback surrounding CSU’s business structure.

“Our decentralized management structure is key to our continued revenue growth. We have experienced management teams operating in each VMS business, backed by infrastructure at the operating group level and a small corporate head office.

The corporate head office provides financial and strategic expertise with respect to capital allocation, acquisitions, finance, tax, and compensation policy, and attempts to identify and share best practices.”

CSU AIF 2024

Acquired companies are there to benefit CSU’s business and CSU’s shareholders, but the founders and managers of the acquired companies get to do what they want. For the most part.

Most small software companies enjoy being acquired, and in a lot of instances, that’s the end goal. And seeing how CSU is seen in the industry as a “homey acquirer” that gives heavy independence and autonomy to acquired companies, it can offer quite enticing arguments to the leaders of the VMS companies it wishes to buy, which may contribute to a lower price paid and/or just smoother buyouts.

Historically, bureaucracy and heavy operating bloat come from integrating acquired companies, especially in large numbers. Most companies with 1,000 technical subsidiaries would be very inefficient at scale. Yet CSU, which has 1,000 subsidiaries, is one of the most well-operated large companies in the world. This is in part because CSU doesn’t reallyhave to operate anything.

Leaving companies untouched following acquisitions and leaving the same people on board that have run the companies since their founding, allows for a founder-operator culture all the way across subsidiaries. Giving these same subsidiaries operational autonomy leads to very little bureaucratic bloat because the subsidiaries end up “operating” themselves.

And to reiterate, they operate themselves with a founder-operator mindset, meaning innovation at the subsidiary level, across most, if not all, companies. And because these managers already know the business they’ve operated for years, CSU can trust them to do a good job managing.

Spoiler: historically, they have.

This, of course, all benefits CSU.

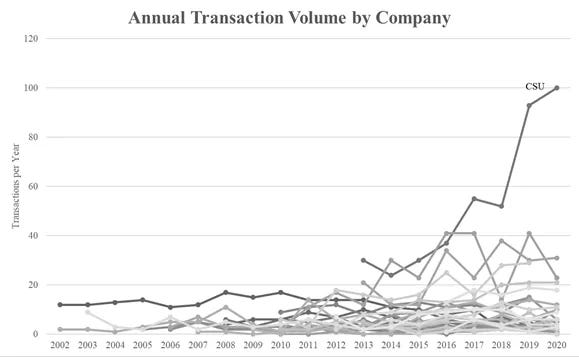

CSU acquires more companies in the “serial acquirer” space than any other in the world, and its growing scale gives it an advantage to continue doing so.

Smooth operational sailing across its subsidiaries = Consistent fundamental growth and/or financial stability. More financial stability = more money to work with = more scale = more acquisitions, and repeat:

The only aspect of the acquired companies CSU dips its hands in, is the financials. (This is to be expected because the acquired company is still, after all, owned by CSU, and tasked with making money for CSU.) So while management and employees are untouched upon an acquisition, CSU can (and does) reach a hand or two into the financial performance of every business, to see where it can use that money to expand.

To explain, say, “Jacob’s Elevator Repair Software,” a CSU subsidiary, made $10m in cash flow in a recent quarter. CSU will take that cash and look across its portfolio for the highest returns to deploy that capital. Now, CSU aggregates the financial results of its subsidiaries into one (it doesn’t list out every company’s results individually), but on an operational level, it needs to decide where to deploy the cash its subsidiaries generate.

Maybe “Jacob’s Graveyard Plotting Software” could use $100m in investment that may lead to more growth. Whatever it is, CSU will constantly recycle capital and invest where there are opportunities. Either to buy more companies, or to help or grow existing companies.

In some cases, CSU will purposely buy companies against its typical strategy if it believes it can turn the business around:

“We prefer to acquire VMS businesses with the following characteristics: Growing business with a diversified customer base, high relative market share and capital constrained competitors.

We sometimes acquire VMS businesses with declining revenue, concentrated customer bases, low relative market share and well-funded competitors. We do so when we believe that the correct combination of customer relationship management and market segmentation will lead to attractive returns.

CSU AIF 2024

While CSU’s “buy more and more companies” business model is the priority, there are areas where some investments into existing companies (to fix inefficiencies, etc) can be done for growth.

“Our VMS businesses typically generate significant cash flows which we redeploy to build our existing VMS businesses and acquire new ones.”

CSU AIF 2024

Much like Brookfield in that sense, CSU is essentially an acquirer of assets that produce cash flow, which it buys through a few intermediaries. (Think of Brookfield Infrastructure buying Brookfield’s infrastructure assets, Brookfield Real Estate buying Brookfield’s real estate assets, and so on.)

Like Brookfield, CSU then uses the cash flow that those acquired assets produce to either buy more assets that produce more cash flow, or invest in existing assets as mentioned above. These business models are nearly the same. The only major difference is Constellation Software’s “assets” are digital, not physical.