Surface-level analyses published before November 10, 2024 are free. For access to newer, fully researched and in-depth reports, consider upgrading to the paid membership.

Hello friends and enthusiasts 👋,

Imagine a world where dollar stores are some of the most profitable businesses on earth. The possibility of a single dollar store chain having a higher profit margin than giants like Walmart and Costco combined while being worth 13x less in market value.

Funnily enough, this isn’t a dream, and chances are, you’ve probably shopped at their stores before.

Today’s a short one, so let’s get into it. (6 min read)

Dollarama: (One of) Canada's Greatest

The biggest retailers in the world usually have terrible profit margins. If they’re lucky, companies like Walmart, Costco, and Loblaws achieve around a 4% margin. Specifically, Costco, whose stock price is up 40% year-over-year, has an average margin of just 2.5-3%.

And that’s to be expected. Retail is a very competitive business.

A low margin is arguably even more expected from Costco since their main business model is giving customers the lowest prices possible and charging them an annual fee for the privilege of having those low prices. Because of this model, around 60% of Costco’s profit comes from their membership.

Then comes Dollarama.

Dollarama is a Canadian dollar store chain that sells a variety of products at low prices, making its business model low-risk with high potential for growth. Dollarama is consistently ranked as one of the best-performing Canadian stocks and has over 1,400 stores across the country. In 2023, Dollarama had an annual revenue of C$6 billion paired with an after-tax profit of C$1 billion.

I’m happy to bet that nearly every Canadian has been to a Dollarama store (sorry Americans). Dollarama’s Costco-like strategy of having the lowest prices and stocking off-label brands similar to the original, has made them a retailer with a profit margin of well over 25%.

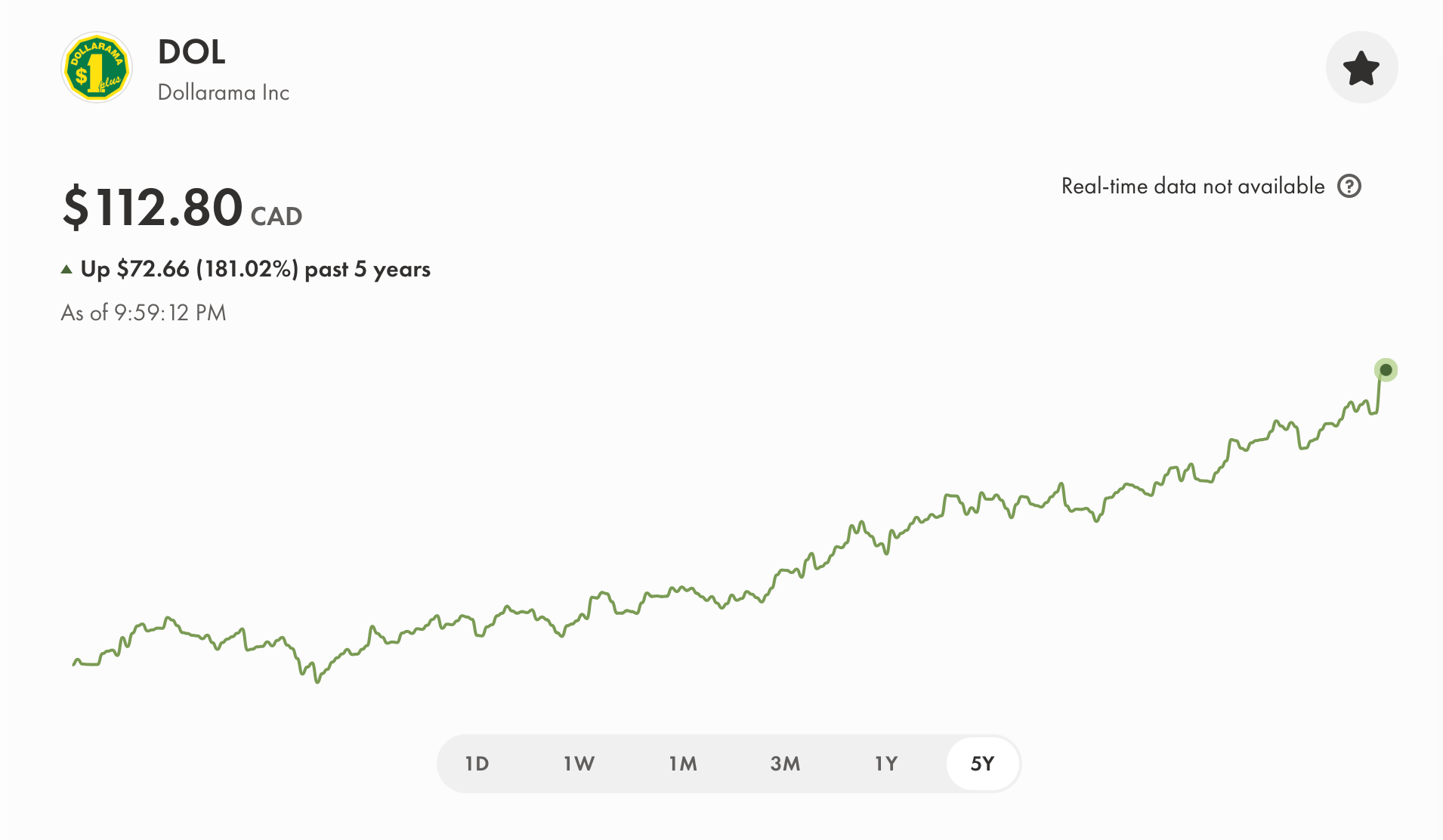

This means Dollarama is not just the most profitable company in North American retail, but it earns a higher profit margin than almost any other retailer on earth. The best part? Its stock price is up over 180% in the past 5 years.

One of the main factors when investing, or even considering an investment in a company, is their moat or competitive advantage. Dollarama’s ~50% market share in the Canadian discount retail market, sizable presence in the Latin American market with a 50.1% stake in Dollarcity, great brand power among consumers, and a 5x industry profit margin already says enough in that aspect.

Since that’s checked off, we can move to the value you, as the shareholder, would gain from investing in the business; in other words:

Is it worth it to buy shares of Dollarama?

To answer this, as with any company, some key aspects to look for are:

Free cash flow (FCF) per share: the amount of cash a business is returning to you on a per-share basis.

Return on invested capital (ROIC): the amount a business is returning you annually for the dollar amount you’re investing.

Compound annual growth rate (CAGR): a metric to determine how much a stock’s price has returned every year over a certain period of time. (CAGR can also be used to determine revenue growth, profit, etc. In this case, I’m using CAGR for stock price because that’s what matters to me and what should matter to most investors.)

For most of my holdings, I prefer a CAGR and FCF per share of 15-20%. Anything less closely resembles an index fund, which would make this whole process not worth it. For ROIC, I like to see anything above 25-30%. Dollarama's stock has had a CAGR of 65% over the past 10 years, and its FCF per share has been growing at 24% over the past 10 years. Its ROIC has been 36% over that same time period.

This means for every $100 invested in Dollarama, they are making $36 for your capital. For comparison, Costco's 22% ROIC, 17% FCF per share, and 52% CAGR in the same time frame is nowhere close. Obviously, that’s nowhere near Apple's 55% ROIC or Mastercard's 49% ROIC, but it’s almost double Costco's ROIC, which is a company over 13x as big as Dollarama.

As always, with every company I add to my watchlist, I run a discounted cash flow analysis (which you can learn how to do here).

Using a 15% growth rate and a 12% discount rate, I came to a fair value of basically C$100.00. (Morningstar says C$96.00). According to my calculation, Dollarama's stock is trading at a premium of 10-12%.

Considering their past track record, I could have used a growth rate of up to 17% or more, which would place Dollarama at fairly valued.

I believe Dollarama is an amazing business, and as much as I would like to invest right now, I believe the price is a little too expensive. And that’s fine with me. As a value investor, patience is the biggest virtue you can have because no matter how good a business is, you don’t want to overpay. Right now, I believe a fair price to pay is C$105.00.

That’s it for today’s Deep Dive. Make sure to check your inbox on Friday for another Weekly Brief. You can read my full Blossom Social post covering Dollarama here.

Let me know your stock suggestions for next week’s Deep Dive by replying to this email or using the comment button below.

Until then, happy investing, and thanks for reading!

☕️ - Jacob xx

While you’re here, here are some other articles you might like: