Just Google It

Google is undervalued, and here's why

Stock analyses/reports published before November 2024 remain free. For access to newer, in-depth reports, upgrade to paid.

Are you familar with Alphabet? As in Alphabet, not the alphabet.

Most average folks aren’t. But considering you’re subscribed to this newsletter, you’re no average folk; you’re most likely a genius. Meaning there’s a high chance you probably already knew that Alphabet is the parent company of Google. (Or maybe it was the title that gave it away… it’s fine, I won’t tell anyone you cheated.)

Google is one of the few major companies in the world to have transformed its business and product name into a literal English verb on a global scale. It’s currently the third-largest company in the world by market cap, the global leader in online advertising, the third-biggest in cloud computing, and supplies the world’s most preferred phone software, email provider, search engine, and entertainment platform. It’s a very intriguingly, growingly diversified technology business that controls the technological lives of billions around the globe.

And as of today, Google stock might also be undervalued.

Google’s Societal Ubiquity

When was the last time you googled something?

Ha, gotcha! That was a rhetorical question.

For most of us, googling something is how we’ve grown to obtain information nowadays. It’s a part of modern-day life. A developed habit some could say. Forget reading books (which is undoubtedly something you should do), tuning in to the 6 p.m. news, or listening to tape recorders. If some piece of information is googleable… well, let’s face it, you’re going to (1) subconsciously eliminate all other options for obtaining that piece of information, (2) pick up your phone, and (3) google it. The catch, of course, is that nearly any piece of information you could ever want to obtain is googleable in today’s world.

But how did we get here? Well, to understand how Google became what it is today, we’re going to take an exciting ride in the Wayback Machine…

A Brief History

Google was created at the beginning of the internet’s rise in popularity, founded in 1998 by Larry Page and Sergey Brin, just three years after the release of Windows 95.

Larry and Sergey were two relatively normal Stanford students minding their own business, studying for Ph.D.s in computer science when they met in 1995. They quickly developed a liking for each other and began working on a research project called “BackRub.” This project did not involve creams and massages; instead, it focused on creating a complex computing algorithm to rank web pages based on importance by analyzing their backlink data. (For those unfamiliar with web development, a backlink is a link on one web page that points to another—a sort of recommendation of web pages if you will.) By 1996, project BackRub was completed, and without knowing it at the time, Larry Page and Sergey Brin had just developed the original Google Search algorithm (now known as PageRank).

Two years later, Larry and Sergey set up the first Google office in the garage of Susan Wojcicki, who was renting out the space to help with her mortgage. Little did Susan know that, with the help of that garage, she had singlehandedly contributed to the revolution of the internet, laying the foundation of a multi-trillion-dollar company.

In 2014, Susan became the CEO of YouTube.

It took Google a single year to reach 1 million users, just five years later to reach 100 million, and only seven years after that to reach 1 billion users. Google’s impeccable timing—launching right at the beginning of the internet’s rapid adoption—allowed it to grow at an almost unprecedented rate following its launch. As Google grew and the adoption of the internet exploded, Google’s active user count followed, with more and more people worldwide associating Google with the internet itself.

Google had become synonymous with the internet, and people like they always do, found a way to colloquialize it. This colloquializing of Google’s name transformed it into a societal ubiquity where today everyone and your grandmother knows what Google is, and what it does.

The even quicker rise of smartphone adaption, paired with Google’s >$20 billion-per-year default search engine deal with Apple’s Safari, extrapolated this colloquializing even further. In fact, if you want something that will blow your mind, at the beginning of this section, I used four colloquialisms related to Google in a single paragraph, and you comprehended the entire thing (google, googling, googleable, and googled). I would not have been able to say those four words just 26 years ago, and that is mind blowing to me.

Today, our world is more online than ever. Google Search is now used by over 3 billion people globally, generating 2 trillion queries every single year. Roughly 60% of the total online population types 2-4 queries to Google every single day.

Onto the Analysis

You’re more than welcome for the Google history lesson, but like all things—and likely the reason why you’re reading this in the first place—money always eventually plays a role. Google is a business trading publicly on the stock market after all, and such businesses need to generate cash for shareholders.

Let’s see, a business with billions of global, recurring attention...

Gosh, Google would make the perfect ad business!

Oh you’ve got to be kidding me—

Alphabet Analysis

Alphabet is the parent company of Google. It was formed back in 2015 as a way for Google to separate its search business from its other ventures while still retaining the Google brand. It’s a weird corporate structure, albeit still completely understandable, because being able to disassociate with a single product is great for a brand’s long-term sustainability and revenue diversification (which you’ll find out below is a huge focus for Google currently). In short: Alphabet is Google playing dress-up, and as you’ve seen throughout this post thus far, I prefer to call businesses what they fundamentally are… which in this case, is Google, not Alphabet.

And that is how I will be addressing them for the remainder of this issue:

Google is an advertising business. It makes money by leveraging the attention of billions of people using its search engine product to attract advertisers that want to sell products to you. Advertising is Google’s core business—it’s their peanut butter and jelly. If you were to add up all advertising-related revenue of the company and express it as a percentage, that number would be roughly 77% of total sales. Most of this revenue is thanks to Search.

However, if you’d like to accurately do justice to Google’s business, saying it’s “just an advertising company” is not the right way to go about things. How I like to look at it is that Google, as a whole, comes together as an advertising business, but the ‘Google sandwich’ is made up of many ingredients. A peanut butter and jelly sandwich, for example, isn’t a peanut butter and jelly sandwich without the ingredients that make it. It involves many separate ingredients that are added together to get the final result. The jam is made of fruit, sugar, and starch; the bread has flour; and peanut butter is… well, peanuts and butter.

I know this sounds silly, but bear with me: Google is a peanut butter sandwich.

Not my best analogy, but hopefully you understand what I’m getting at.

Google is one thing at the end of the day: one particular business. But underneath it all, if you look at it from a broader perspective, there are many different factors that make that “one business” one of the best businesses in the world. Then of course, there is innovation. Room to swap out the flavour of jam every so often, or change from crunchy to smooth peanut butter, and what have you.

Google has for years been the de facto leader in online search. (More on this below in the competitive advantage section). We’ve covered this briefly today, but what we haven’t covered is how effectively Google managed to diversify its revenue using the massive reach of its search business. As I covered in Weekly Brief #47 a couple weeks back, all major tech companies became successful because of a superior business model. Since these companies are so unfathomably massive on a global scale, it’s only a matter of time before these superior businesses eventually stagnate in growth. That’s a no-no for investors in the technology sector. So, these companies leverage their superior business model(s) to diversify into other sources of revenue.

Luckily, the management and executive teams of big tech are usually just as superior as the businesses they operate, which is one of the most remarkable aspects of them. The management of Google spotted this future growth stagnation decades before it began to take place, and as soon as they could, steered Google on a path of revenue diversification. This path led to Google’s groundbreaking acquisitions of YouTube, DoubleClick, and Android, which are ranked among the most successful acquisitions of all time. These three acquisitions together alone are now responsible for what is today, 20% of Google’s total revenue.

Google’s long-time employee-first workplace environment also ended up being a major player in this path of revenue diversification, particularly in the story of Gmail, which was created by a Google engineer as an internal side project (more on that another day). At the time, big email provider names like Yahoo! and Hotmail were providing very small amounts of storage for free, meaning users had to constantly delete old emails to free up storage so they could send more. It was a hassle, so when Google launched Gmail to the public in 2007 and offered 1 GB of free storage—400 times more than the big players at the time—people flocked to the platform. Gmail has been the most favoured email provider in the world since, and is currently used by over 1.8 billion people.

Over time, this revenue diversification strategy had proved successful for Google like it had for most of big tech. (Thanks to high Research and Development (R&D) investments, powerful and successful acquisitions, and the many successful consumer products and services). After 26 years, Google shifted its business from making 100% of its revenue from online search to just ~57% of its revenue from online search by diversifying into cloud computing, subscriptions, expanding the Google Ads network, leveraging its Search reach to launch hundreds of successful consumer apps, services, and products, while also developing the first autonomous driving rideshare service that actually makes money (sorry, Tesla).

Google Cloud, YouTube Premium, Google Workspace, Gmail, Chrome, the expansion of its third-party advertising services, Waymo, Pixel, Nest, Google Maps… it’s a seemingly endless list of highly successful products, services, and apps.

Google doesn’t need to make money from all of these apps or services. In fact, most of them are not fully monetized, and I believe that’s purposeful. The non-monetization of these highly popular products and services helps explain the huge (77%) revenue share from advertising. Speaking realistically based on reach and usage of the products here, that metric could be changed at the snap of Google’s fingers.

By leveraging the massive reach of Google Search and perfectly crafting products to be attractive and value-packed, Google funnels billions of people from Search into their suite of products, entering those users into an ecosystem that not only makes it seamless to use other Google products but also makes the consumer that much more likely to stick with and continue using Google Search over the long term. If you’re using Gmail, have a YouTube account, and use Google Maps, Google is training your brain to be constantly familiar with Google and its services, helping you become attached to the brand and maintain the dominance of the business.

With the dominance of the search business and the massive amount of data Google now has on you from your use of its many services, Google can advertise to you more effectively, thereby making more money off you. Google’s ability to gather so much data from a variety of products and services and sources is what gives Google its world class advertising platform and global market domiance.

Even though Google wants and needs to diversify its business, it still needs the support of Search to grow and obtain resources to maintain its ecosystem and invest in diversifying revenue. And that my fellow investors, is where R&D comes in.

Google’s AI Strategy

Since the launch of ChatGPT, companies have made a big push into LLMs, racing to be the leader in the new technological revolution of artificial intelligence.

AI spending at Google has hit somewhere near $14 billion per year as of the time of writing, mostly related to cloud architecture spending (Nvidia chips) and building out data centres. This spending is hurting Google’s free cash flow greatly, which has led investors (me included) to wonder if this spending will actually yield returns.

Here’s how Google CEO Sundar Pichai responded to investor sentiment surrounding the massive amount of spending on AI:

“We may overspend on AI, but the risks of not spending enough are higher.”

Most of Google’s AI spending is focused on building out its data centre capabilities to improve its cloud computing offerings (similar to what the other cloud giants, AWS and Azure, are doing). This is the main focus for Google at the moment. Google Cloud is the fastest-growing revenue segment of Google by far, and the cloud computing market growth is on an exponential uptrend along with it.

Secondarily, with the remainder of the spend, Google is investing heavily in developing AI models and LLMs. Google’s eventual plan in this area is to incorporate these models into Pixel hardware, Google Workspace, and the many other products, apps, and services Google offers, to enhance capabilities and improve the value proposition. Unlike OpenAI, which is the current undisputed leader in the AI model and LLM space, Google has much more user data to train these models and has been developing AI for over a decade.

OpenAI is falling short, or will eventually fall short, of data to train its models. What this means in the end for OpenAI, is high licensing costs to get hands on more data. Google does not have this problem and, quite frankly, probably never will.

Artifical intelligence, if put in a single word, would be data—and Google has a lot of it.

Remember those many popular products and services that Google owns and the 2 trillion(+) annual Search queries Google processes every year? With those alone, Google has an almost endless source of data in its current position.

When you download a free app from Google, they still pay for the costs of running it. Google isn’t in the business of hand outs—Google is in the business of making money. In this particular case, even though the app is free, you are, every day, paying Google. Not monetarily of course, but with your data. All for the convenience of their wonderful suite of free*, value-packed products. This is why Google keeps these apps free. They want the data. They need the data to help broaden their AI training abilities, highten advertising campaigns, and make more money.

Unique queries, billions of users using their data-farming products every single day, and a technological grip on so many people’s lives… it’s an incredible cycle.

In terms of data, I believe Meta is the only on-par rival to Google in terms of companies that have already released a LLM. Both Google and Meta are laying the groundwork to become leaders in AI models and LLMs over the next decade or longer, thanks mostly to the unique data they have. ChatGPT may be the most advanced LLM currently, but I believe that eventually, with the resources Google has, the experience they have in developing consumer technology, and the immense amount of data they control, Google will be an inevitable winner in the AI revolution alongside Meta in the LLM space.

(Amazon, too, is an extremely powerful data company—potentially even more powerful than Google and Meta, combined (not a typo). I purposely left it out here because they have not launched an LLM as of the time of writing, though it is in production. I thought it was worth mentioning regardless.)

Much like Amazon and Meta, although not as significant, Google has incredible revenue diversification opportunities ahead.

Google’s revenue is broken down as follows (TTM1):

Google Search (56.9% of sales)

Online search advertising revenue and ads earned from Google subsidaries such as Gmail, Google Maps, and Google Play.

Google Cloud (11.4% of sales)

Subscriptions (11.3% of sales)

Revenue generated primarily from Google’s subscription services (i.e., YouTube Premium, Google Workspace, Google One), as well as from Google’s platforms and hardware technology products like Pixel, Chromebook, Google Home, and Nest.

YouTube Ads (10.3% of sales)

(Self-explanatory.)

Google Network (9.4% of sales)

Revenue generated from ads served on third-party websites and apps using Google AdSense and other Google-affiliated commercial ad products.

Other Bets (0.56% of sales)

Revenue earned from Google’s side projects. This includes Waymo (autonomous driving), Verily and Calico (healthcare subsidiaries) and any other bets, as the name suggests.

Fundamentals, Moat, Growth, Valuation

Fundamentals

One of the things I love about big tech is the predictability of its absolutely stunning business fundamentals. When you hear the phrase “big tech,” you know you're entering the territory of the most profitable, consistent companies on the planet. While some arguably inconsistent companies are sometimes lumped into this category (coughs, Tesla), there’s usually a sizeable fine line between big tech companies and everything else.

Google is no exception.

Here’s a look at some of Google’s key fundamental metrics from the past five years (definitions for the abbreviations are listed at the bottom of this post):

Revenue CAGR3: 17.21%

Earnings CAGR: 20.33% (22.96% per share)

EBITDA4 CAGR: 20.28%

FCF5 growth: 17.02% (19.60% per share)

Dividend increased: N/A

Shares outstanding: -10.71%

Profit margin: 26.70%

Operating margin: 32.40%

ROCE6 (average): 21.76%

My favourite metric to look at is FCF. Why FCF and not earnings or EBITDA or anything else? Because you can’t buy anything with earnings, but you can with cash. FCF represents the cash a business generates, making it the best way to value a company. For Google, FCF growth over the past five years has been remarkable. On a per-share basis, which typically ends up reflecting in the stock price, FCF has been growing at an average rate of 19.60% per year—nearly double the market.

Google is a fundamentally pristine business.

Google’s competitive advantage

Google is the predominant leader in search, where it controls roughly 92% of the market. It’s an advertising behemoth with an incredibly wide moat. But aside from search, Google also holds significant shares and leads in many other niche, important markets, such as:

Mobile OS (Android): 71%

Total global online advertising: 29%

Cloud computing (Google Cloud): 11%

Browser market (Chrome): 66%

Autonomous driving/robotaxi (Waymo): Percentage-wise, N/A; however, Waymo is by far considered the leader in this market.

Regulatory scrutiny: This year, however, has been challenging for Google’s moat. In August, the U.S. Department of Justice won a case deeming Google an illegal monopoly, stating that it violated antitrust laws and abused its scale to harm consumers and businesses. Just last week, Google was hit with a court order to open up its app store to rivals, and we learned that the U.S. Justice Department may soon ask a judge to break up the company. This has scared many investors, causing the stock to drop roughly 22% from its highs in June.

As a reminder to investors who are reading this and fearing a potential breakup, while it definitely seems alarming at first glance, a breakup might actually turn out to be a bonus for you as a shareholder. The many individual companies Google owns will almost surely be valued at a much higher valuation when they’re individually owned rather than wholly owned by Google.

Remember, as a Google shareholder, if this breakup happens, you’re going receive shares of these split-up companies (or in cash if it’s taken private). It’ll be an extremely bad thing for Google as a company, but it might not be a bad thing for you as an investor (assuming the market treats the valuations of the post-split companies relatively fairly). While I can’t predict the outcome, I don’t believe this will be a major hurdle for Google in the long term. Currently, the odds are against Google, but even with this disadvantage, I believe Google will hold strong. Hopefully the DOJ thinks attentively, and uses rational thought and keeps Google together. But I don’t believe they will go through with it.

Growth aspects & valuation

According to analysts, over the next five years, Google is expected to grow revenue by 9%, earnings by 12%, and free cash flow (FCF) in the same range (I believe FCF per share will be around 13-15%+).

Much of this growth will be driven by Google’s expanding cloud revenue, subscription revenue, advancements in AI models and LLMs, as well as continued growth in search and YouTube (and potentially even autonomous driving (more below).

There are three main markets Google has entered that are projected to grow exponentially and consistently over the next decade. These will be the intrinsic value drivers for Google over the next decade and longer:

Cloud computing (Google Cloud):

Online advertising market growth (Search, YouTube etc.):

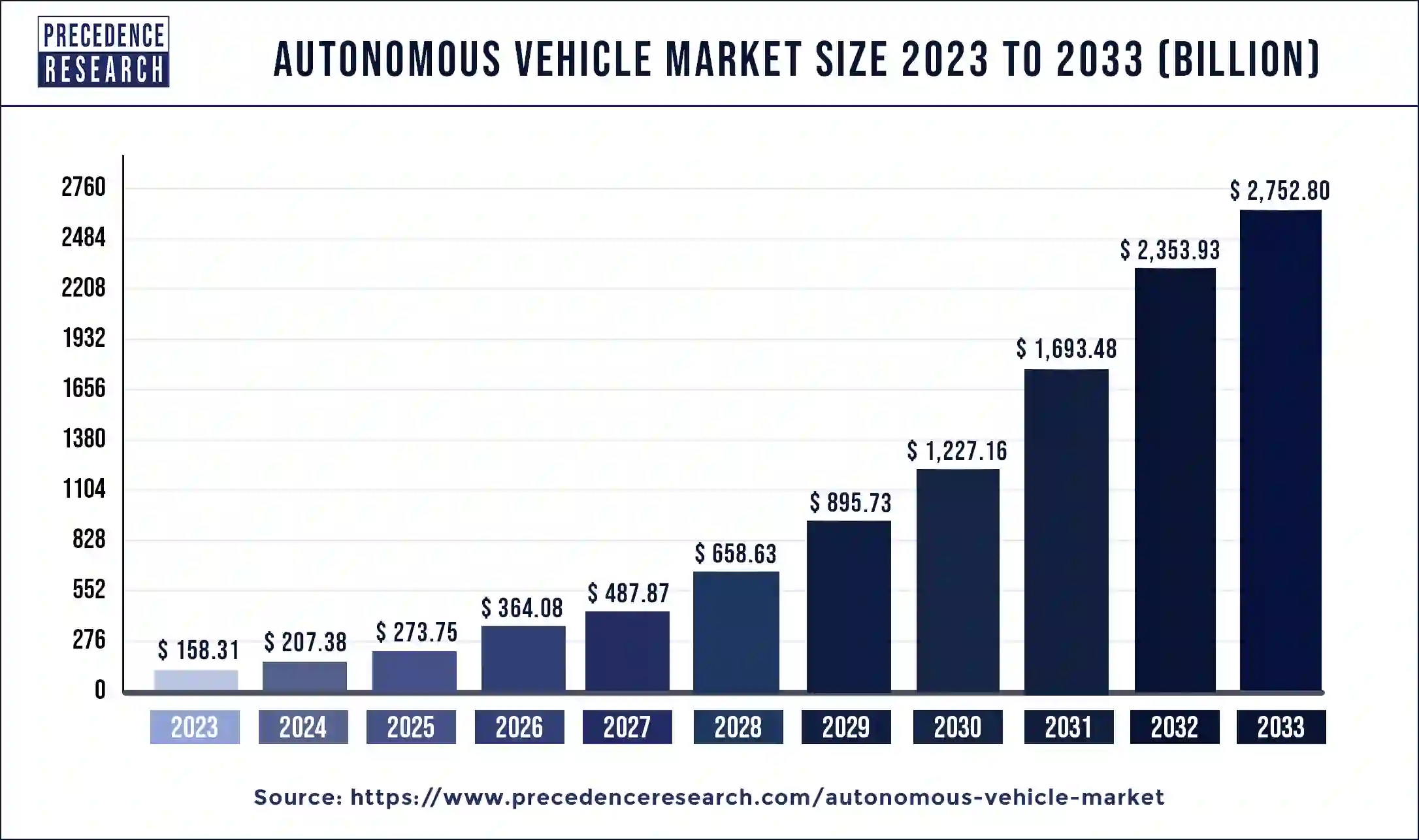

Autonomous vehicle market growth (Waymo):

I can’t accurately determine Waymo’s current market share in autonomous vehicles and robotaxis, but according to a few sources, Waymo is currently the clear winner in the market, (and that’s at a premature stage in the business). I can only assume that, over the long term, Google will continue to be a leader due to its familiarity, continued innovation, and operations in the industry, and will benefit greatly from this explosion in the autonomous vehicle market on the revenue side. The recent partnerships with Uber and Hyundai only help back this argument up.

For cloud and online advertising however, I can determine market share meaning that by 2032, Google will take in $718 billion in revenue from those two segments based on its current 11% share in cloud and 30% share in global online advertising. Assuming its market share stays where it is.

With all the investments in AI, as mentioned above, Google’s free cash flow has been taking significant hits. Usually when I value a business, I run a discounted cash flow analysis and compare multiples. While I could definitely use multiples here, given the current volatility in FCF, I believe its best to use operating cash flow (OCF) in this situation. Currently, using a DCF that substitutes Google’s FCF with OCF, with a growth rate of 13%, a discount rate of 15%, a margin of safety of 30%, and a terminal multiple of 25 (Google’s average) over the next five years, I get a fair value of approximately $1.903 trillion, or roughly $152.00 per share. This puts Google at around fair value based on today’s prices.

I can already hear the thoughts…

“Jacob, this is an extremely conservative assumption. Google is undervalued!”

I would agree. As an alternative valuation path to give an idea, I averaged Morningstar’s current fair value rating of $209.00 per share with my estimate, to get a fair value of around $181.00. I’m not saying either of the two numbers are correct, because a DCF is the least important thing with respect to valuing a business, so do with this information as you will. But it should give a rough estimate ($152-181).

My thoughts: Based on current metrics, Google is trading at a 5.25% OCF yield and an 18 forward P/E ratio. Looking at these metrics and some of Google’s other multiples compared to history and other notable competitors in the industry (Meta, Amazon, Pinterest), and factoring in the potential future returns of the AI spending, cloud growth, a growing product subscription revenue, autonomous driving, and secular consistent online advertising growth, while also adding into the picture everything meaningful I mentioned throughout this write-up, I believe Google is currently undervalued, and I see Google stock as a buy at today’s levels.

—-

Thank you for reading. Happy investing.

Trailing twelve month (TTM) data at the time of writing.

Cloud or cloud computing is the offering of computing services over the internet. The cloud (which is colloquialism for the internet, not an actual cloud), allows users to access and use servers to store databases, networking, software, and analytics without the need for physical hardware or infrastructure. Simply put, it’s a digital storage centre for data. Think of Netflix or Dropbox or iCloud — all of these services and more depend on the capabilites of cloud computing services to store and manage their data.

Compound annual growth rate (CAGR): a metric to determine how much a stock’s price has returned every year over a certain period of time. (CAGR can also be used to determine revenue growth, profit growth, etc.)

Earnings before interest, taxes, depreciation and amortization (EBITDA).

Free cash flow (FCF): the money left over to shareholders after subtracting a business’s operating income by its capital expenditures.

Return on capital employed (ROCE): a financial ratio used to assess a company’s profitability and capital efficiency. Helps understand how well a company is generating profits from the money it spends.

Excellenty explained

Excellent write-up and analysis. I really enjoyed this!