Weekly Brief #79

UnitedHealth is falling, should you buy?... Plus, Canadian Tire acquires Hudson’s Bay, Middle East invests $2.5 trillion in U.S, Uber launches fixed-route shuttle, U.S., China pause tariffs, and more.

Good morning investor 👋,

Welcome or welcome back to the 79th Weekly Brief—the quality investor’s weekly market recap.

This week’s performance:

S&P 500: +4.18% | Nasdaq: +6.05% | Dow Jones: +2.22% | TSX: +2.29% | Gold: -3.25% | Bitcoin: -0.42% | The Quality Fund: +7.69%.

Markets are surging, and so is morale, after the U.S. and China finally reach a trade deal. But what’s not up? UnitedHealthcare stock, the once 15th largest publicly traded company on planet Earth—now 37th, down ~$300 billion in market cap within the span of a month. Simple question: should you buy?

Let’s get into it. (12 min read)

In this issue:

📉 UnitedHealth stock is falling, should you buy?

🤝 Canadian Tire acquires Hudson’s Bay

🇺🇸/🇨🇳 U.S. and China pause tariffs

FEATURED STORY

📉 UnitedHealth stock is falling, should you buy?

I was going to name this title: Is UnitedHealth a juicy investment right now?

And, well, that depends on how you define “juicy” in this context.

For me, a “juicy” deal is one where you’re catching a falling stock price of a terrific, outstanding business with minimal disruption or overblown risks leading to the downturn. Much like Amazon in March–April of 2025 (now that’s juicy).

When you’re buying a depleting stock, you can either buy a falling tennis ball or a falling knife. Both hurt, but one has a soft fall, and the other leads to injury1.

What’s undeniably true is that UnitedHealth needs medical attention. In a month; down over 53%.

Just in the past month, the company has (1) experienced its first earnings miss since 2008, (2) cut quarterly guidance, (3) suspended annual forecasts, and (4) is being investigated by the DOJ for medical fraud (though this investigation report has been confirmed misleading by UnitedHealth). The cherry on top? Its current CEO also resigned.

I’ve noticed a flow of opinions on the internet as this crash became mainstream in investing communities. And there lies the simple but important question I wanted to tackle in this post: Is UnitedHealth a buy?

It really is a great business

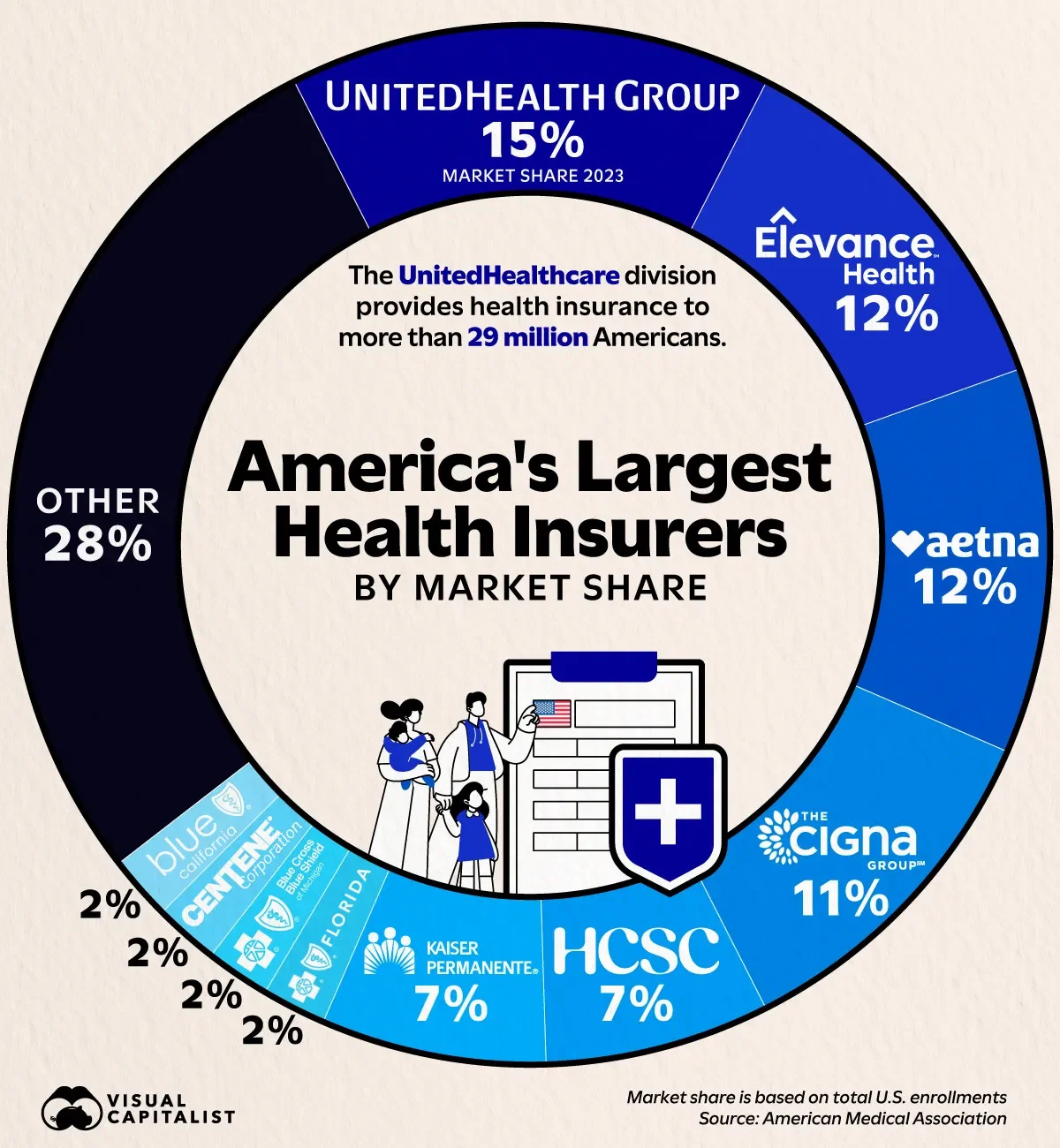

UnitedHealth, or UnitedHealthcare depending on the context, is the largest health insurance provider in the United States. (Because, unfortunately, unlike in Canada where your tax dollars are the insurance premiums, Americans need to pay a company for the luxury of potentially having a doctor’s visit covered.)

I don’t want to assume I understand the American healthcare system, because I’m not even sure Americans understand the American healthcare system. So if you don’t like my judgement here, please keep this in mind.

However, I do understand business.

And when a business goes on sale, my eyes perk.

To start, UnitedHealth is undeniably trading at a cheap price.

As I write this, it’s trading at a 10.52x forward P/E, a 0.61x P/S, and a ~10% FCF yield. Historically, its median multiples of these same metrics are 21.89x for P/E, 1.19x P/S, and a 5.78% FCF yield.

But we must include context for this massive selloff.

When a company pulls its full-year guidance and its CEO resigns shortly thereafter, the company has no idea where it’s headed. These P/E metrics could be much worse than today. The E in P/E could change drastically over the next year. Who knows. None of the reasons for the drop explained above, on their own, are catastrophic. But together? That’s not irrational market noise. That’s a problem.

Valuation is great. But what if valuation is just catching up to what the business is actually worth? Who’s to say a health insurance company should be valued at 20x earnings in a normal situation?

Here’s what Bill Ackman had to say back in February of this year (well before the 50%+ drop):

If we look at some of UnitedHealth’s main competitors (Cigna, Elevance), the average historical P/E is about 10x.

From what I can see, UnitedHealth seems to be the better compounder. It is and has always grown faster than its competition, and is much more consistent. It does deserve a slight premium to the industry in my eyes. Including when UnitedHealth’s strength isn’t just its insurance premiums.

One of the main arguments I’ve heard—especially in Twitter replies2 in the past week—as justification for holding/buying this stock is:

“Well, UnitedHealth isn’t just insurance, it has care delivery and pharmacy management too (Optum)!

Vertical integration!”

And this is true: UnitedHealth has a few revenue segments. Here’s the revenue breakdown for you, as of Q1 2025:

Premiums (77.4%) (insurance)

Products (12.5%) (pharmacy)

Services (8.8%) (healthcare services and tech)

Investments (1.3%)

UnitedHealth has an amazing business model despite the many current fundamental setbacks, I’ll give them that. They are the leading major insurance provider in the U.S., and they were one the first to my knowledge, to use this dominance in an incredibly effective way—branching out and integrating products and services to build more powerful revenue streams, and a stronger business as a whole.

In U.S. healthcare, there are three main players:

The insurer who pays the bills

The pharmacy who fills the prescriptions, and

The doctor/clinic who gives the treatment

Elevance and Cigna (again, main competitors of UnitedHealth) are mainly just the insurers—UnitedHealth is all three players.

This is what those “Twitter bros” mean when they talk about UnitedHealth’s vertical integration. It took me about an hour to wrap my head around this, but not only does UnitedHealth insure you; they manage your prescriptions with OptumRx, run the clinics you visit with OptumHealth, and even build the software hospitals use (OptumInsight).

This is what justifies a slight premium.

They have an amazing business; the shareholder’s dream.

At this point you may be wondering why my thoughts have been so positive. And well, that’s where that ends.

Should you buy?

The reasons above that made UnitedHealth a strong and powerful company, is what made them attract hatred. Hatred means negativity.

And you’re an investor, so negativity is your kryptonite.

Having this almost monopolistic-like grip on the healthcare industry due to its complex network and integration has meant use of pricing power and generally unethical practices to collect dimes.

Say… I don’t know… higher fees for pharmacy delivery? Or rejecting a tad too many insurance claims to save out on payouts? Yes, there is evidence to support UnitedHealthcare unjustifiably rejecting necessary health coverage to its clients. Particularly elderly clients rejected by their AI systems.

… Say hello to American capitalism.

The many cases of unethical business practices and consistent price increases has led UnitedHealth to severe backlash.

You may remember from six months ago (December 2024) when the prior CEO of UnitedHealth, Brian Thompson, was allegedly killed by Luigi Mangione.

If you look at the comment sections or reposts of any clip or mention of this murder, the comments are 70% thanking the killer, 15% saying “he shouldn’t have been killed, but he was an evil person at an evil company so,” and 15% “this was awful.” Absolutely no one likes this company.

Or the service it provides.

Or the people that run it.

The hatred is like none I’ve ever seen.

And I wouldn’t dare to bet against the hatred of consumers. I wouldn’t dare to invest directly into hatred no matter how attractive the valuation or business.

It’s not that the company itself is bad per se. As an investor, the business and current valuation is attractive. But the American healthcare system is overly political, and the concerns I mentioned in the first section above paint a grim fate for the company in the near term.

I don’t believe much of this screams “juicy” deal, by my definition.

I stand by my philosophy that a successful business wins long term by providing value to its customers. Those are the businesses I wish to invest in.

My thoughts: I would stay away. Too much uncertainty. Too many negatives. Too political of an industry. Sure, a great business—arguably great valuation. And maybe in the very very long term (10 or 20 years+) this stock won’t be affected. But policy moves fast, and this potential DOJ probe mixed with turbulent management and all-over-the-place financial reporting is not a great picture if you’re looking to invest.

If you are, prepare for flat or negative returns for a long while—assuming things go exactly back to normal with time.

That’s it, folks. Thank you for reading. Happy investing.

Upgrade to the paid membership to read this week’s final Q1 exclusive earnings reviews (in the Discord), and to have full access to next week’s premium stock report on MercadoLibre. I hope to hear from you soon.

More to read in the meantime:

FINANCE

a. 🤝 Canadian Tire acquires Hudson’s Bay

Canadian Tire is set to acquire Hudson’s Bay’s… branding assets—including its iconic stripes, logos, and coat of arms—for just $30 million, pending court approval. Hudson’s Bay has been under creditor protection since March, and plans to close all 80 Bay stores and 16 Saks locations by the beginning of June.

The company is 355 years old, and has been American-owned since 2006. Canadian Tire CEO Greg Hicks called the move “an honour,” saying it preserves a piece of Canadian heritage. Liquidation asset sales are underway. It’s great that at least the brand will continue to live on another day.

b. 💰 Middle East invests $2.5 trillion in U.S.

Over Donald Trump’s recent Middle Eastern “Gulf tour” three nations have pledged a combined $2.5 trillion in investments for/into the U.S. Here’s the breakdown from largest to smallest:

🇦🇪 UAE: $1.4 trillion over 10 years (primarily into tech, AI, and energy)

🇸🇦 Saudi Arabia: $600 billion (lots of weapons, AI data centres (via AWS and others), and more)

🇶🇦 Qatar: $200–300 billion (Boeing jets, defence, and infrastructure)

If you’ll notice, these three countries are heavily dependent on oil exports to fuel their economies. These countries in particular have been working to heavily divest from oil and diversify their economies. And what better way to diversify than to spend money growing their own tech sectors and cozying up to a U.S. president who loves the sound of dollar signs? This is bullish for all parties.

Related articles:

BUSINESS

c. 🚌 Uber launches fixed-route shuttle

Uber is officially rolling “Route Share,” a new feature offering 50% off fixed-route rides during weekday commutes in seven major U.S. cities, including NYC, Chicago, and San Francisco. Riders can pre-book shared trips with up to two people along preset routes running every 20 minutes. This is a very exciting step for Uber as they venture to build trust and affordability for consumers in a strong but worrying economic situation like 2025.

“People feel uncertain and overwhelmed… They want more affordable options, and we’re focused on delivering them.” — Uber CPO Sachin Kansal.

Uber hopes to eventually have Route Share expanded to autonomous vehicles (AV) and to qualify for commuter benefits. As I write this, Uber is already in-partner with ~18 AV companies and plans to host shared AV rides with Volkswagen in L.A. by 2026. Huge news.

Related articles:

d. 🏭 Amazon invests $5 billion in Saudi Arabia

Amazon, in partnership with Saudi AI company Humain, is expected to invest over $5 billion into infrastructure, servers, training programmes, and tools to help support local start-ups to build an “AI Zone” in Saudi Arabia.

Humain is funded by the Public Investment Fund (PIF), Saudi Arabia’s state-owned investment fund, and has also partnered with tech giants like Nvidia and AMD. Other companies indirectly partnering with Humain include Google, Salesforce, and Oracle (which have partnered with the PIF). This announcement is in addition to Amazon’s $5.3 billion existing Saudi data centre project, set to launch in 2026. Though the dollars might overlap.

Related articles:

MACRO

e. 🇺🇸/🇨🇳 U.S. and China pause tariffs

After meeting in Geneva for two days of talks, U.S. and Chinese officials announced a deal on Monday to roll back most of the barbaric tariffs for 90 days to allow further negotiations. U.S. Trade Representative Jamieson Greer said the U.S. would “reduce its tariff rate on Chinese goods from 145% to 30%,” and China would lower its rate on U.S. goods to 10%.

China’s Commerce Ministry said both sides agreed to “cancel 91% of existing tariffs and suspend another 24%,” totalling a 115%-point reduction. Treasury Secretary Scott Bessent said neither side wants “a decoupling,” and he warned that previous tariff levels would have completely blocked trade (which we’ve known)—nearly $700 billion in annual trade, for that matter.

The current reductions do not apply to autos, steel, aluminum, or any new pharmaceutical tariffs (if there are any).

Personally, I feel this pause isn’t enough. And I hope both sides can be rational about this matter and negotiate this tariff war down to irrelevancy over the coming months. The world’s two superpowers economically fighting it out—this isn’t what the world needs. But in the meantime, I’ll take the ~+8% in a week.

Related articles:

📚 Book of the Week

For every book purchased using the links below, 100% of affiliate commissions are donated to charity. (Amount donated so far: $36.42.)

An investor’s bookshelf: Here.

Mastery - Robert Greene

Book Description:

Each one of us has within us the potential to be a Master. Learn the secrets of the field you have chosen, submit to a rigorous apprenticeship, absorb the hidden knowledge possessed by those with years of experience, surge past competitors to surpass them in brilliance, and explode established patterns from within. Study the behaviours of Albert Einstein, Charles Darwin, Leonardo da Vinci and the nine contemporary Masters interviewed for this book.

The bestseller author of The 48 Laws of Power, The Art of Seduction, and The 33 Strategies of War, Robert Greene has spent a lifetime studying the laws of power. Now, he shares the secret path to greatness. With this seminal text as a guide, readers will learn how to unlock the passion within and become masters.

Thank you for reading, partner. If you enjoyed today’s issue, share it with friends and family. I’ve placed a button below for you to do so (right underneath the paid membership line (see what I did there).

All the best,

Jacob

All of my links here.

My best work is members-only. Don’t miss out on exclusive posts, insights and benefits—upgrade today and join the community.

Sure, you could injure yourself with a falling tennis ball, but you get the point!

(I’m barely on Twitter, it was a fling)

I have no opinion about (or understanding of) UNH, but using the same logic of generalized hatred would have prevented you from investing in a long list of highly profitable companies such as Philip Morris and/or Altria (before their separation, the best investment compounder ever according to H. Bessenbinder’s study), any of its competitors, and just to name a few, Manville (acquired by W. Buffett’s BRK), John Malone’s cable companies on their many incarnations and spinoffs, Nelson Peltz’ consolidation of the asbestos-plagued metal can industry, even Mallinckrodt that was a high-flyer for years before its true nature was revealed.

Been buying UNH. I don't understand the CDN health care system..waiting 9 months for a MRI or 2 years+ for a knee or hip replacement 🤔 can you even call that a health care system?